What's new for tax year 2021 ACA Reporting? | AIR

1. New ACA Codes added to the Form 1095-C

The two new codes (1T - 1U) in Line 14 to report the method they used to determine the affordability

of ICHRA Coverage.

Code 1T: This code applies when an individual coverage HRA (ICHRA) was offered to an employee and spouse

without dependents. The affordability of the plan was determined using the Zip Code of the employee's primary residence.

Code 1U: This code applies when an individual coverage HRA (ICHRA) was offered to an employee and spouse

without dependents. The affordability of the plan was determined using the Zip Code of the employee's primary employment site.

2. 30-Day Extension of Form 1095-C Reporting Deadline

The IRS announced it was extending the deadline for distributing Form 1095-B and 1095-C to individuals from

January 31st to March 2nd.

For paper filers, the deadline is February 28, 2022. Electronic filers have until March 31, 2022.

What's new for tax year 2020 ACA Reporting? | AIR

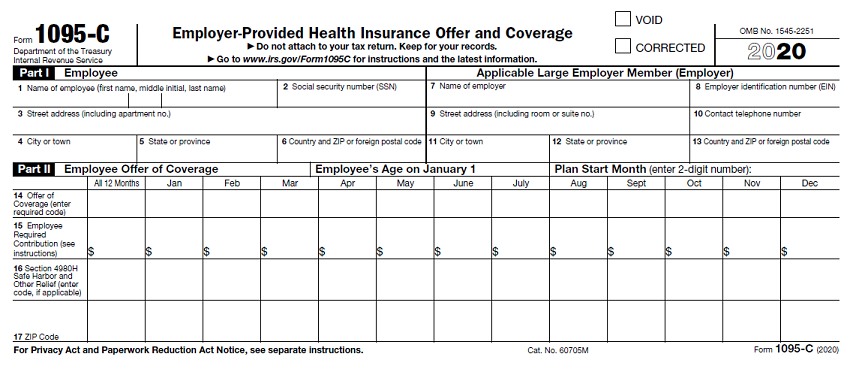

Additions to Reporting for Form 1095-C

IRS Form 1094-C remains unchanged from prior years.

IRS Form 1095-C tax year 2020 changes include a new line 17, new offer codes and box for employee's age.

Form 1095-C is now a 2 page form where Boxes 1-17 are listed on page 1 and the covered individuals are shown on page 2.

- Employee's age: The IRS will now require an entry for the "Age" of each employee as of January 1, 2020. This will be in

Part 2 on the 1095-C form. Use either an age or the full birth date of our 1099FIRE software will automatically calculate

the date of birth as of January 1.

Employee age will only need to be completed by employers who utilized individual coverage health reimbursement arrangements. Otherwise, age can be omitted.

Age appears in Column X on the 1095-C excel spreadsheet. - New offer codes: In part two of the 1095-C form, a new Box (17) has been added to report information relative to the Health Reimbursement

Arrangement (HRA). They have provided new codes to use relative to this type of coverage IF you offer it. These additional codes are

1L through 1S and used in Box (14).

1L. Individual coverage health reimbursement arrangement (HRA) offered to you only with affordability determined by using employees primary residence location ZIP Code.

1M. Individual coverage HRA offered to you and dependent(s) (not spouse) with affordability determined by using employees primary residence location ZIP Code.

1N. Individual coverage HRA offered to you, spouse and dependent(s) with affordability determined by using employees primary residence location ZIP Code.

1O. Individual coverage HRA offered to you only using the employees primary employment site ZIP Code affordability safe harbor.

1P. Individual coverage HRA offered to you and dependent(s) (not spouse) using the employees primary employment site ZIP Code affordability safe harbor.

1Q. Individual coverage HRA offered to you, spouse and dependent(s) using the employees primary employment site ZIP Code affordability safe harbor.

1R. Individual coverage HRA that is NOT affordable offered to you; employee and spouse or dependent(s); or employee, spouse, and dependents.

1S. Individual coverage HRA offered to an individual who was not a full-time employee. - New line 17: If any codes 1L through 1Q are used in Box (14), a corresponding zip code is required in section 17.

New State Filing Requirements

Prior to 2019, the ACA required individuals to maintain qualifying health coverage, or pay a penalty if they did not qualify for

an exemption. However, the 2017 Tax Cuts and Jobs Act reduced the ACA individual responsibility penalty to zero, effective

January 1, 2019. In response, some states and the District of Columbia (D.C.) have enacted a state-level individual health

coverage mandate and associated penalties. Many employers will have a role in the enforcement of these mandates, as providers of

health coverage.

Health Coverage Mandates Effective in 2020

Effective January 1, 2020, taxpayers in the following states: California, the District of Columbia (D.C.), New Jersey, Massachusetts, New Jersey, Rhode Island, and Vermont are required to maintain minimum essential health coverage or potentially pay a penalty.

What does this mean for you?

The states adopting the mandate requiring individuals to carry coverage will need a way to validate

that an employee has coverage either on the exchange or through their employer. If insurance is coming from

the employer, the validation is coming through as a state tax form. Although your business may not reside

in one of these states, there still may be employees that claim residence.

These individual states are mandating 1095 reporting to their state agency in addition to the IRS Federal filing.

The states are taking this seriously. New Jersey has already distributed letters to companies that did not comply

and the other states will follow suit.

1099FIRE is the only service bureau which offers state filing on behalf of their clients.

This is an outsource service only. For more information please call (480) 706-6474.