1099 Software: How can I efile replacements?

How can I efile replacements?

One frequently asked question is “I put together a new file, there are 0 potential errors, I click Transmit and I see..”

and the Replacement option is grayed out. The software can not automatically transmit a replacement like it would an original or correction because you have to find the file in the IRS FIRE System that you want to replace. To do this:

- Create a new fire.txt file and double check that there are no errors.

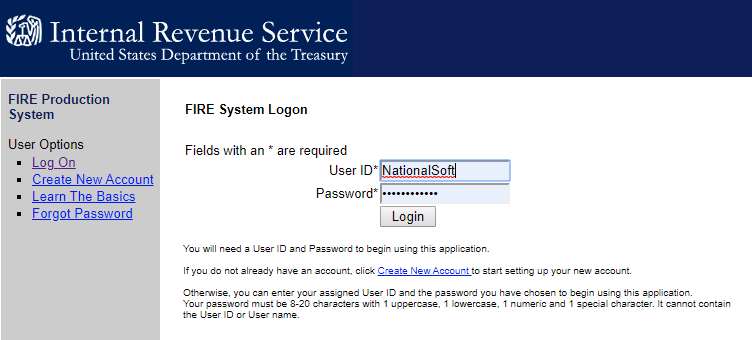

2. Log into fire.irs.gov:

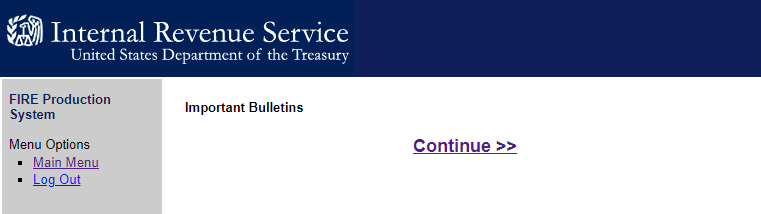

and click Continue to go to the Main Menu or click Main Menu to the left.

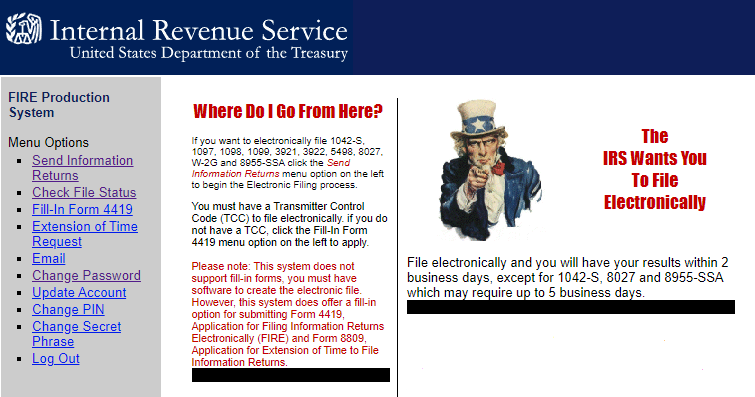

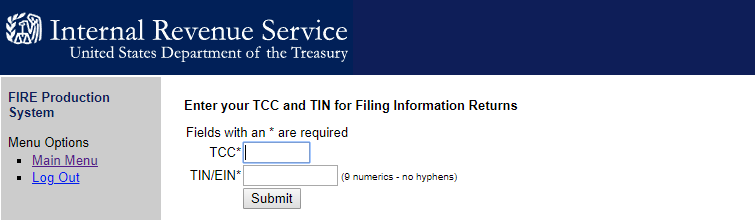

3. At the Main Menu Options, click on Send Information Returns which is to the left.

4. Type in your TCC and EIN for the transmitter.

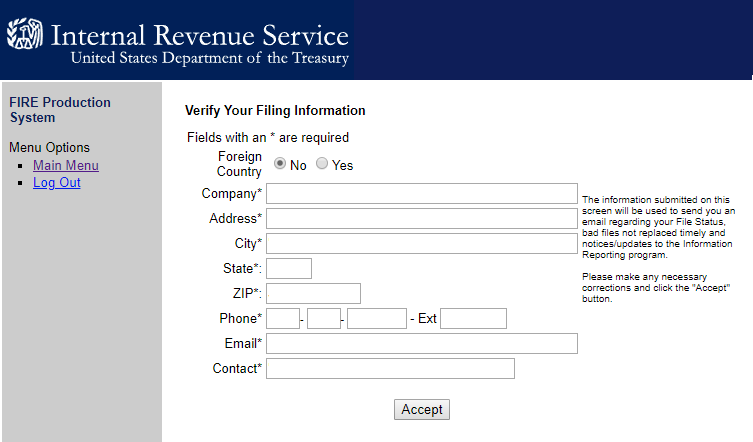

5. Verify your transmitter information and click Accept.

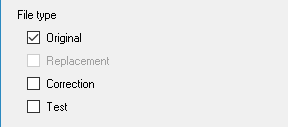

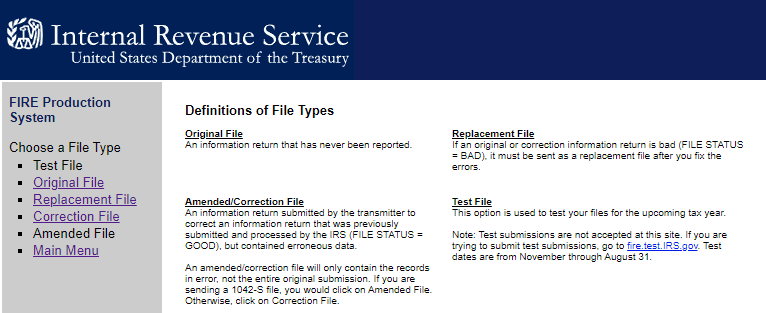

6. You will be asked to choose a file type. Here you can select Original, Correction or Replacement. Select Replacement.

7. You will see a list of files needing replacement. There may be only one file to replace. Select the file you want to replace.

If you uploaded many originals that came back as “Bad” and you only want to replace one of them, then you need to call the IRS and ask them to delete the other “Bad” originals.

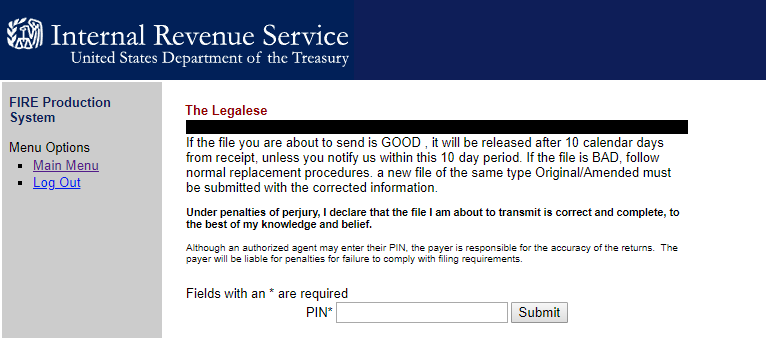

8. Type in your PIN.

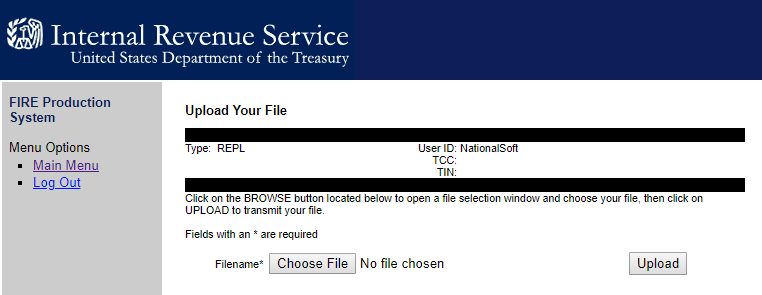

9. Click on Choose File and find the replacement file and then click Upload.

What is a replacement file?

A replacement is a new original file. If you submit a file to the IRS and it comes back as “Bad“, then the file does not exist in the IRS FIRE System. You want to replace the bad file with a new original file. You can replace an original or correction and you get credit for the date/time in which you submitted the original bad file. If you submitted the original file on or before a due date, you can submit a replacement within 30 days and its still considered on time.

30 days to file a replacement

Something was wrong with the file that you submitted. To find out exactly what errors as associated with the file that you submitted, log into the IRS FIRE System and go to the Main Menu and click on Check File Status. Find your file and click on it and the IRS will show you the errors associated with your file.

1099FIRE Service Bureau

We efile on your behalf. We do charge for that service. Just call sales at (480) 460-9311 to get started.